Blockchain technology is essentially a digital ledger. Think of it as a notebook where every transaction or data exchange is recorded. Unlike a physical notebook, this digital version is duplicated across thousands of computers globally, making it nearly impossible to alter. This technology became famous with Bitcoin, a digital currency. Yet, its potential goes much further.

Table of Contents

Imagine tracking your morning coffee’s journey from the farmer to your cup. Or voting from your living room, confident that your vote is secure and counted. Blockchain promises to transform industries, from finance to healthcare, by offering a method to record and share information that is secure, transparent, and efficient.

What is Blockchain Technology?

Imagine a record-keeping book that’s not kept in one place but copied and spread across a network of computers. Whenever someone adds a new page to this book, everyone’s copy gets updated. This is the essence of blockchain technology. It’s a way of storing information in a manner that makes it tough to cheat, hack, or change the system. At its heart, blockchain is a chain of blocks, but not in the traditional sense of those words. Here, “block” refers to digital information (the transactions) stored in a public database (the “chain”).

Blockchain technology offers a decentralized platform. This means it doesn’t rely on a single central point of control. A good analogy is a shared document or spreadsheet duplicated thousands of times across a network of

computers. The network is designed to regularly update this document, ensuring all copies are the same and true.

This technology came into the spotlight with the rise of digital currencies like Bitcoin, but it’s proving to be useful far beyond, creating a foundation for a new type of internet. Originally designed for the digital currency, tech communities are finding other potential uses for the technology.

Why is Blockchain Important?

Blockchain technology has sparked widespread interest across various industries. Its appeal goes beyond supporting digital currencies such as Bitcoin. Blockchain offers a revolutionary approach to conducting transactions, sharing information, and securing data. Here are key reasons why blockchain is considered a transformative technology:

Enhanced Security: Blockchain introduces multiple security layers not found in standard computer files or network systems. It encrypts data and spreads it across a network. This distribution makes it challenging for hackers to access the information. Each transaction undergoes recording, verification, and security in this distributed ledger, minimizing the risk of unauthorized access and fraud.

Increased Transparency: The level of transparency blockchain provides is unmatched. All transactions are recorded and visible to every participant in the network. This visibility promotes trust and accountability, crucial in sectors where transaction integrity matters, like finance and supply chain management.

Reduced Costs: Blockchain technology diminishes the need for intermediaries, such as banks or lawyers, in various processes. This reduction in middlemen cuts costs. By simplifying transactions and using smart contracts for automation, businesses can save on time and operational expenses.

Faster Transactions: Traditional banking transactions, especially international ones, can take days to complete. They are prone to errors and delays. Blockchain operates around the clock, allowing for quicker processing times. Transactions can occur within minutes or seconds, unaffected by holidays or weekends.

Improved Traceability: Blockchain ensures that every transaction is recorded and traceable. This feature benefits supply chain management, enabling companies to trace the origins of goods, verify their authenticity, and comply with regulations. This traceability also helps prevent fraud in trading and ensures the legitimacy of traded items.

Blockchain stands as a pivotal technology for its security, transparency, cost efficiency, speed, and traceability. These attributes make it an essential tool in transforming how businesses operate, enhancing their efficiency, and fostering trust in transactions.

History of Blockchain

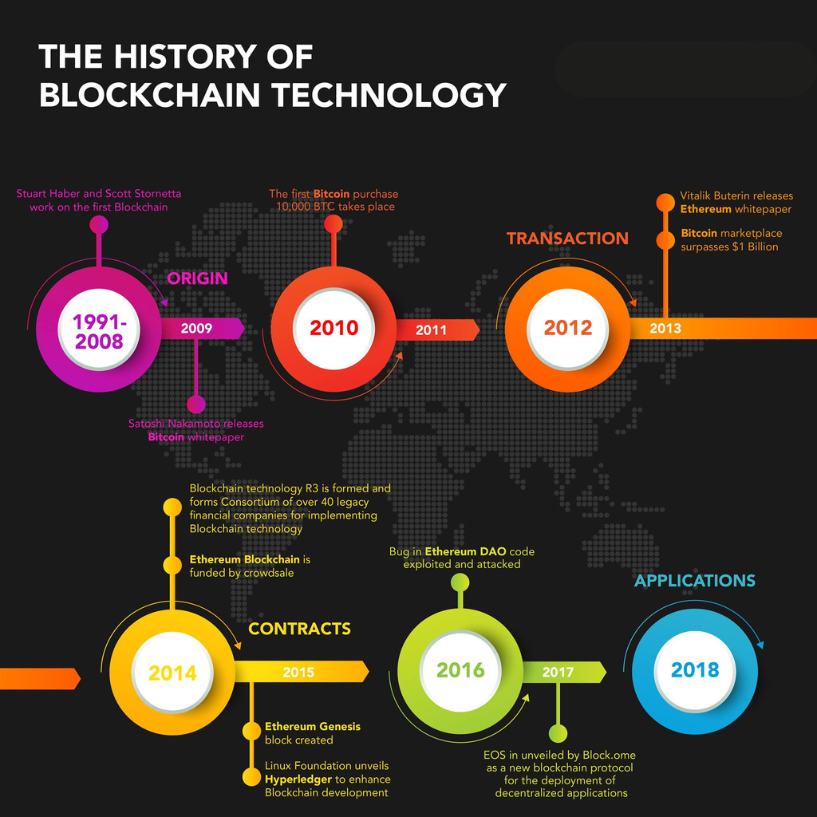

The roots of blockchain technology stretch back farther than many realize. To grasp its history, we venture back to 1991. It was then that Stuart Haber and W. Scott Stornetta first introduced a method to timestamp digital documents. Their goal was to prevent backdating or tampering. This concept laid the foundation for what would eventually become blockchain technology.

However, it wasn’t until 2008 that the blockchain, as we know it today, was conceptualized. An individual or possibly a group, using the pseudonym Satoshi Nakamoto, presented the idea. It served as the backbone for Bitcoin, a digital currency designed for transactions without central authority oversight. This concept was groundbreaking. It proposed a system to record transactions securely, transparently, and permanently on a decentralized network.

The publication of the Bitcoin white paper, “Bitcoin: A Peer-to-Peer Electronic Cash System,” ignited interest in blockchain’s potential beyond Bitcoin. The concept of a decentralized, secure, and transparent transaction recording method attracted attention from various sectors, including healthcare, supply chain, and governance.

Evolving Beyond Bitcoin

Bitcoin introduced blockchain to the world. Yet, the technology’s potential applications quickly emerged beyond digital currencies. In 2015, Ethereum, initiated by Vitalik Buterin and others, built on Bitcoin’s foundation. It introduced smart contracts, which are self-executing contracts with the terms of the agreement directly written into code. This innovation automated contract execution and enabled the development of decentralized applications (DApps).

This shift redefined blockchain from a technology for financial transactions to a platform for decentralized applications across industries. Today, blockchain’s exploration and adoption in supply chain management, healthcare, digital identity verification, and more showcase its versatility. It has the potential to revolutionize digital interactions.

Key Milestones in Blockchain History

1991: Stuart Haber and W. Scott Stornetta lay the conceptual groundwork for blockchain.

2008: Satoshi Nakamoto conceptualizes the first blockchain for Bitcoin.

2009: The launch of Bitcoin marks the first application of blockchain technology.

2015: The introduction of Ethereum expands blockchain’s uses with smart contracts.

Blockchain’s history illustrates the swift evolution of technology. It highlights the potential to reshape not only financial systems but various societal aspects.

How Do Different Industries Use Blockchain?

Blockchain technology, initially crafted for Bitcoin, now transcends its original scope. Diverse sectors adopt blockchain to address challenges in security, transparency, and efficiency. Here’s an overview of blockchain applications across industries:

Finance and Banking:

Payments: Blockchain facilitates quicker, cost-effective, and secure international transactions, bypassing traditional intermediaries.

Fraud Reduction: Transparent and secure transaction logs on blockchain minimize fraud risks.

Smart Contracts: Automating contracts with blockchain cuts intermediaries, lowering costs.

Supply Chain Management:

Provenance Tracking: Blockchain enables real-time, transparent tracking of product origins, aiding in authenticity and compliance.

Reducing Counterfeits: It verifies product authenticity, curbing counterfeit goods in the supply chain.

Healthcare:

Patient Records: Blockchain ensures secure, efficient management of patient records, accessible only to authorized individuals.

Drug Traceability: It tracks pharmaceuticals from production to delivery, ensuring safety and compliance.

Voting Systems:

Security and Transparency: Blockchain can create a secure, transparent electronic voting environment, potentially reducing fraud and boosting turnout.

Real Estate:

Property Records: Blockchain simplifies property title and record transactions, enhancing transparency and speed.

Tokenization of Real Estate: It allows fractional ownership and trading of real estate, similar to stock exchanges.

Education:

Credential Verification: Securely stores academic credentials for easy verification by employers or institutions.

Energy Sector:

Decentralized Energy Grids: Blockchain facilitates decentralized energy grids for direct energy trade among users, improving efficiency and possibly reducing costs.

Blockchain’s adaptability opens up vast possibilities across fields, fostering innovation and efficiency.

Industry giants recognize blockchain’s transformative potential. Jamie Dimon of JPMorgan Chase and former IBM CEO Ginni Rometty have praised its ability to reduce transaction costs, speed up processes, and enhance supply chain transparency and efficiency.

As blockchain technology evolves, we anticipate its expanding role in revolutionizing various sectors, underscoring its significant, broad impact.

What are the Features of Blockchain Technology?

Blockchain technology is renowned for its unique attributes that address common issues in digital transactions, such as security, transparency, and efficiency. Delving into these attributes helps us understand blockchain’s broad applications across various industries. Below, we explore the key characteristics that distinguish blockchain technology:

Decentralization:

Unlike traditional databases, such as a bank’s ledger which is centralized and controlled by one entity, blockchain spreads its data across a network of computers. This structure ensures that no single failure point can compromise the data’s integrity. The decentralized nature of blockchain enhances its resistance to censorship and external threats.

Transparency:

Blockchain maintains transparency while safeguarding user identities through secure cryptographic keys. Every transaction on the blockchain is accessible to network participants, rendering any attempt to modify transactions highly detectable by others.

Immutability:

After recording a transaction on the blockchain, it becomes permanent. This feature guarantees the transaction history’s integrity, positioning blockchain as the optimal ledger for trust-dependent transactions.

Security:

Blockchain achieves high security through a consensus process for transaction approval and the encryption and linkage of each transaction to the preceding one. Its decentralized framework further secures it against fraudulent activities and unauthorized alterations.

Reduced Transaction Costs:

Blockchain cuts transaction fees by eliminating intermediaries required for transaction verification. This reduction is particularly beneficial in sectors like financial services and international trade, where intermediaries traditionally claim a significant share of the profits.

Efficiency and Speed:

Conventional transaction methods, especially for international dealings, can be cumbersome. Blockchain technology, by automating and streamlining these processes, ensures faster and more efficient transactions.

Programmability:

Through smart contracts, which are self-executing contracts with the agreement terms embedded in code, blockchain enables automated workflows. This feature facilitates applications that operate without downtime, fraud, or third-party interference.

The convergence of these features positions blockchain as a potent instrument for revolutionizing not only financial transactions but also various business and governmental operations. It enhances security, transparency, and efficiency, heralding a new era in how transactions and processes are conducted.

What are the Key Components of Blockchain Technology?

Understanding blockchain technology means knowing its key parts. These components ensure transactions are securely logged, checked, and kept over a decentralized network. Below are the vital parts of any blockchain system:

Block: A block is the smallest unit in a blockchain and holds data. It stores details of transactions, including the sender, receiver, and the amount transferred. Each block has a unique identifier known as a “hash,” setting it apart from others.

Chain: Blocks connect in a specific sequence, forming a chain. Each block points to the hash of the one before it, creating a time-ordered trail of data. This structure safeguards the blockchain’s integrity, as altering any information would mean changing all subsequent blocks, a near-impossible task.

Node: A node is a computer connected to the blockchain network. Its jobs include validating,

storing, and distributing blocks. All nodes have the blockchain’s entire history, updated with new blocks as they are approved and attached.

Consensus Mechanism: This method achieves agreement on transactions’ validity across the network’s nodes. Blockchains employ different consensus mechanisms, like Proof of Work (PoW) or Proof of Stake (PoS), to protect the network and confirm transactions.

Cryptography: Blockchain relies on cryptographic methods to secure block data. This ensures only those with the correct private key can access the information, offering privacy and security.

Smart Contracts: These are automated contracts whose conditions are coded directly into the blockchain. Smart contracts execute on their own when conditions are met, eliminating the need for central authorities or external enforcement.

Distributed Ledger Technology (DLT): Blockchain is a form of DLT, recording transactions with an unchangeable cryptographic signature, a hash. Any alteration in a block is immediately noticeable, making blockchain resistant to fraud and hacking.

These components unite to form the secure and resilient system blockchain is celebrated for. They support various uses, from financial dealings and supply chain oversight to verifying identities, transforming our approach to data security and exchange in the digital age.

How Does Blockchain Work?

To understand how blockchain technology operates, we must explore the journey of a transaction from initiation to its inclusion in the blockchain. This explanation simplifies the intricate process involved.

Transaction Initiation:

The journey begins with a user sending a digital currency to another. This step involves specifying the digital addresses of both the sender and receiver, alongside the amount being sent.

Transaction Verification:

For a transaction to join the blockchain, nodes or network participants must verify it. The blockchain might employ different verification methods, such as Proof of Work (PoW) or Proof of Stake (PoS).

Forming a Block:

After verification, the transaction is grouped with other recently verified transactions to form a new block. Each block not only contains transaction data but also a unique code, or hash, and the hash of the preceding block in the chain.

Adding the Block to the Chain:

This new block must be appended to the existing blockchain. A consensus mechanism ensures multiple network nodes agree on the validity of the block’s transactions and its hash. This consensus prevents any single entity from manipulating the blockchain.

Permanence and Transparency:

Once a block is part of the chain, it’s permanent and immutable. Blockchain’s key feature is this immutability. While transactions on the blockchain are transparent and open for viewing, the identities of the participants remain protected and anonymous.

Proof of Work vs. Proof of Stake:

Proof of Work (PoW): A consensus mechanism requiring participants to solve complex problems to verify transactions and create blocks. The first to solve the problem adds the block to the blockchain and receives a reward. Bitcoin uses PoW.

Proof of Stake (PoS): As an alternative to PoW, PoS allows users to verify transactions and create new blocks by holding and staking cryptocurrency. It’s considered more energy-efficient than PoW.

Ensuring Security and Trust:

Blockchain’s design and cryptographic techniques render it highly secure. Its decentralized nature eliminates any single point of failure, enhancing network security. The consensus requirement for transactions ensures accurate recording and verification by multiple parties, building trust.

This groundbreaking method of recording and sharing data has revolutionized secure and transparent transactions across various sectors, redefining our approach to online security and data integrity.

What are the Types of Blockchain Networks?

Blockchain technology showcases a remarkable flexibility, extending its utility far beyond the realm of cryptocurrencies. Its applications span various domains, including business and governance, attributable to its diverse network types. Each type presents unique characteristics, determined by access permissions and specific use cases. This exploration reveals the primary blockchain networks:

Public Blockchains

Public blockchains stand out as open, decentralized platforms. They welcome anyone to engage in pivotal activities such as transaction verification and logging. Bitcoin and Ethereum exemplify public blockchains, celebrated for their transparency and security. These networks depend on consensus protocols like Proof of Work (PoW) or Proof of Stake (PoS). These mechanisms foster trust and integrity within the network.

Private Blockchains

In stark contrast, private blockchains are permissioned networks under the stewardship of a single organization. Access is exclusive, extended only through invitations, with the central authority holding the power to rescind participation privileges. These blockchains boast enhanced transaction speeds and privacy. However, their centralized nature sparks debate. Critics argue this centralization strays from the foundational principles of blockchain technology.

Consortium Blockchains

Consortium blockchains emerge as a semi-decentralized alternative, governed by multiple organizations. This setup offers a balanced approach, blending the openness of public blockchains with the restrictive access of private networks. Such arrangements are particularly beneficial in collaborative business ventures among competitors. They share a blockchain to safeguard transparency and security without relinquishing control to a singular entity.

Hybrid Blockchains

Hybrid blockchains ingeniously merge the characteristics of both public and private networks. They provide a framework for private, permissioned activities alongside the option to publicly share specific data. Businesses find this blend attractive for conducting confidential transactions with the assurance of transparency and security for selected information on a public ledger.

Understanding these blockchain types illuminates the technology’s versatility. It demonstrates blockchain’s potential to innovate and streamline processes across a multitude of sectors, making it a cornerstone technology for the future.

What are the Benefits of Blockchain Technology?

Blockchain technology brings several advantages due to its unique features. These include decentralization, transparency, security, and being unchangeable. These traits can change many sectors. They do this by making transactions more efficient, secure, and trustworthy. Below is a look at the main benefits:

Enhanced Security

Blockchain keeps data very safe through complex cryptography. Each transaction gets encrypted and linked to the one before it. This forms a chain that’s hard to alter. This high level of security is vital in areas like finance, healthcare, and others dealing with sensitive information.

Increased Transparency

Transaction histories are clearer with blockchain. It works as a shared ledger. All who are part of the network see the same data, not just individual copies. Updates to this shared version need everyone’s agreement. This process ensures data is accurate and open.

Improved Traceability

Blockchain provides a record that traces a product’s origin and its journey. This is crucial for confirming a product’s authenticity and fighting fraud. It’s particularly useful in pharmaceuticals, luxury items, and agriculture.

Reduced Costs

Cutting costs is crucial for businesses. Blockchain reduces the need for middlemen since trust is placed in the blockchain data, not in the trading partner. This can lower expenses significantly for large-scale operations.

Increased Efficiency and Speed

Blockchain makes processes less reliant on

paper, less prone to error, and removes the need for middlemen. It automates these processes, making transactions quicker and more efficient. Blockchain works all day, speeding up banking activities that could otherwise take days.

Automation Capability

Blockchain allows for the use of smart contracts. These contracts execute automatically when conditions are met. This lessens the need for manual processing and quickens transactions.

The use of blockchain is vast. For instance, it makes the supply chain more transparent and traceable. This lets buyers know where their purchases come from. In finance, it makes transactions quicker, cheaper, and safer. In healthcare, it allows secure sharing of medical records, improving patient care and data safety.

Leaders in various fields see the potential in blockchain. Jack Ma of Alibaba talked about its ability to build trust in a trustless world. He noted its power to change the global economy. Christine Lagarde from the European Central Bank pointed out its role in making financial markets more innovative and inclusive.

As blockchain grows and develops, its benefits are likely to increase. This could offer more transformative possibilities in many more sectors and uses.

What is the Difference Between Bitcoin and Blockchain?

Understanding the relationship between Bitcoin and blockchain is crucial for comprehending the scope of digital currencies and the technology that supports them. Despite common confusion, Bitcoin and blockchain are not synonymous. Each stands for a distinct concept.

Bitcoin

Definition: Bitcoin represents a form of digital currency, known as a cryptocurrency, which came into existence in 2009. An anonymous figure, using the name Satoshi Nakamoto, introduced it. This currency allows for transactions from one person to another without the need for central oversight by banks or governments. Its design emphasizes decentralization, aiming to serve as an online medium for purchases and as an option for investment.

Purpose: The fundamental goal of Bitcoin is to provide an alternative to traditional currencies. It seeks to enable safe, clear, and swift international transactions without intermediaries.

Blockchain

Definition: Blockchain technology is the backbone of cryptocurrencies, including Bitcoin. It’s a system for recording information across a network of computers. This setup ensures that records are secure, transparent, and unalterable.

Purpose: While blockchain supports Bitcoin and other cryptocurrencies, its potential extends further. It promises a secure and effective way to log transactions and manage assets in various fields. These include finance, healthcare, and supply chain management.

Key Differences

Scope: Bitcoin is a cryptocurrency. Blockchain is the foundation technology not only for Bitcoin but also for many other applications.

Function:Bitcoin serves as a method of payment and a value storage. Blockchain is a system for recording data and transactions securely and transparently.

Application: Bitcoin’s use is mostly in finance as a digital currency. In contrast, blockchain technology finds applications in numerous sectors. These range from healthcare to supply chain management and beyond.

Innovation:Bitcoin introduced the notion of a decentralized digital currency to the world. Blockchain technology, however, signifies a novel approach to data and transaction management. Its potential applications extend well beyond the realm of digital currencies.

While Bitcoin operates as a digital currency enabling direct transactions, blockchain serves as the revolutionary technology that allows Bitcoin and myriad other applications to exist securely and efficiently.

Why is Blockchain Popular?

Blockchain technology has seen a remarkable surge in interest from various sectors over the last decade. This enthusiasm stems from its unique features that promise to transform traditional ways of conducting transactions, securing data, and establishing trust in digital communications. The main reasons for the growing popularity of blockchain include:

Decentralization

The decentralized nature of blockchain stands out as one of its most compelling attributes. Unlike traditional systems, it operates without a central authority. This aspect minimizes the risks associated with data manipulation, censorship, and control by a single entity. It offers an unprecedented level of transparency and security, appealing to a wide audience.

Enhanced Security

Blockchain employs sophisticated cryptographic techniques, ensuring data integrity and protection against hacking. Industries that prioritize data security, like finance, healthcare, and government, find this feature particularly beneficial.

Trust in Transactions

Blockchain’s transparency and immutable record-keeping foster trust among users. Every transaction is visible and unchangeable once recorded. This characteristic is vital in fields like supply chain management, where the ability to verify a product’s journey from origin to consumer is essential.

Cost Reductions

Blockchain streamlines operations and reduces the need for intermediaries, cutting down transaction costs and administrative expenses. This efficiency is especially valuable in international trade and finance, where traditional transactions can be expensive and slow.

Innovation and New Opportunities

Blockchain paves the way for innovations such as decentralized finance (DeFi), non-fungible tokens (NFTs), and decentralized autonomous organizations (DAOs). These new models have attracted significant investment and attention, further propelling blockchain’s popularity.

Smart Contracts

Smart contracts execute automatically based on set rules without intermediaries. This capability is revolutionary for various sectors, automating and simplifying processes like insurance claims and royalty payments, making them more efficient and less costly.

Global Interest and Investment

The global commitment to blockchain, from governments to private entities, underscores its potential to disrupt established business models and open up new opportunities. This widespread support has brought blockchain to the forefront of technological innovation.

Public and Media Attention

The media’s focus on blockchain, especially its connection to cryptocurrencies like Bitcoin, has played a crucial role in its popularity. While sometimes leading to misunderstandings of blockchain as solely a financial tool, this coverage has also broadened the conversation about its potential far beyond the realm of finance.

Blockchain’s increasing popularity reflects its ability to tackle core issues of trust, transparency, and efficiency in today’s digital world. As it continues to develop, its applications are expected to grow, further establishing its transformative impact on the digital economy.

Pros and Cons of Blockchain Technology

Blockchain technology is at the forefront of digital innovation, offering a mix of benefits and challenges. Understanding these is vital for anyone considering blockchain solutions. Below, we explore the major advantages and obstacles:

Pros

Security: Blockchain stands out for its security measures, including encryption and the interconnected nature of its blocks. This feature is particularly important in fields like finance and healthcare, where safeguarding sensitive data is paramount.

Transparency: The technology’s distributed ledger ensures unparalleled transparency. Every transaction is open to view and verification by all network participants, fostering trust.

Efficiency and Speed: Blockchain eliminates the need for intermediaries, thanks to smart contracts. This streamlines transactions, notably in international dealings, enhancing speed and efficiency.

Reduced Costs: By cutting out middlemen and speeding up transactions, blockchain lowers costs. This makes various services more economical and accessible.

Immutability: Recorded transactions on the blockchain are permanent. This unchangeable nature guarantees the integrity of transaction histories, crucial for trust-sensitive activities.

Cons

Complexity: The underlying technology of blockchain is intricate, posing comprehension challenges for many. This complexity can slow its acceptance and integration into current systems.

Scalability: Issues of scalability plague some blockchain networks, especially those reliant on Proof of Work (PoW). These limitations can cause delays and increased fees during high-traffic periods.

Energy Consumption: PoW-based networks, such as Bitcoin, draw criticism for their substantial energy use, sparking environmental concerns. New consensus mechanisms, like Proof of Stake (PoS), aim to mitigate this issue.

Regulatory Uncertainty: The legal landscape for blockchain and cryptocurrencies is in flux, with varying levels of regulation worldwide. This inconsistency can deter adoption and investment.

Integration Challenges: Merging blockchain technology with existing business systems and processes can be daunting and expensive, necessitating extensive IT and operational adjustments.

blockchain technology’s benefits—security, transparency, efficiency, cost reduction, and immutability—are compelling. However, the challenges it faces, including complexity, scalability, energy consumption, regulatory uncertainty, and integration difficulties, must be addressed for it to achieve broader acceptance.

The Future of Blockchain Technology

The future of blockchain technology is on a path of significant growth and innovation. This evolution could reshape numerous industries by offering methods to conduct transactions and manage data that are more secure, transparent, and efficient. Looking forward, we can anticipate several developments that will influence the progress of blockchain:

Wider Adoption Across Industries:

Industries beyond finance, such as healthcare, supply chain, real estate, and energy, are starting to implement blockchain solutions. These solutions tackle various challenges, from tracking the origin of products to securely handling patient records. As the advantages of blockchain gain recognition, its use is expected to expand across different fields.

Integration with Other Emerging Technologies:

Blockchain is set to merge more closely with other cutting-edge technologies like the Internet of Things (IoT), artificial intelligence (AI), and 5G networks. This convergence could unveil new functionalities, for instance, AI-managed smart contracts or secure, decentralized data sharing among IoT devices.

Advancements in Scalability and Sustainability:

Scalability remains a major hurdle for current blockchain networks. Future efforts will likely focus on crafting blockchain systems that are both more scalable and environmentally friendly. Innovations may include new consensus mechanisms such as Proof of Stake (PoS), sharding, and layer 2 solutions like Lightning Network and sidechains.

Increased Regulatory Clarity and Standardization:

As blockchain technology advances, we can expect the establishment of clearer regulatory frameworks and standards. This development will not only provide legal clarity for companies and users but also aid in preventing fraud and ensuring the security of blockchain transactions.

Growth of Decentralized Finance (DeFi) and Non-Fungible Tokens (NFTs):

The DeFi sector and the NFT market are poised for further growth. These areas highlight blockchain’s capacity to renew existing systems and forge new economic models.

Enhanced Privacy Features:

With rising concerns about data privacy, future blockchain platforms are likely to include advanced privacy features. Technologies like zero-knowledge proofs could allow for transactions and interactions without disclosing sensitive information, thereby offering greater privacy and security.

Cross-Chain and Interoperability Solutions:

The ability to interoperate between different blockchain networks will become increasingly crucial, enabling smooth exchanges of information and value. Solutions that facilitate cross-chain interactions will improve the utility and efficiency of blockchain technology.

Despite facing challenges like scalability, energy consumption, and regulatory barriers, blockchain technology’s ongoing development and inherent benefits point towards a promising future. As blockchain continues to evolve, it is expected to profoundly influence our digital interactions, leading to a digital future that is more secure, transparent, and equitable.

Blockchain has traveled from its inception as a support for digital currency to a technology with the potential to revolutionize various sectors. With expected greater innovation and adoption in the years ahead, blockchain is transitioning from a disruptive technology to a foundational component of the global digital infrastructure.

Conclusion

Blockchain technology, initially designed for Bitcoin, has become a pivotal innovation across numerous sectors. Its key features—decentralization, transparency, immutability, and security—tackle major challenges in digital transactions and data management. Blockchain is revolutionizing finance with cryptocurrencies and DeFi, enhancing supply chain visibility, and protecting personal data. Its future holds wider adoption and deeper integration into established and new areas. Addressing scalability, energy use, and regulation is crucial for its advancement. Blockchain’s synergy with AI, IoT, and 5G could vastly improve digital infrastructures, making them more efficient, secure, and fair.

Blockchain is a cornerstone of modern digital infrastructure, symbolizing a shift towards transparency, reliability, and efficiency. Its evolution from a novel concept to a transformative technology illustrates the impact of innovation in expanding the realm of the possible.

Looking forward, blockchain’s development is not just about technological progress. It represents a move towards a digital society where transactions and data sharing are safe, transparent, and universally accessible. The ongoing embrace and enhancement of blockchain technology are steps towards a decentralized, democratic digital future.